Can your stimulus check be taken away by debt collectors?

The newest stimulus check may create some questions or doubts about your current or upcoming bankruptcy process. Our experienced bankruptcy attorneys answer all of your stimulus bankruptcy questions.

Do I get to keep my stuff in bankruptcy?

Exemptions can help protect your property in a bankruptcy case. It is important to talk to a bankruptcy attorney near you who can help you understand the plan best for you and show you how the benefits of bankruptcy will work out in your unique case.

How to Keep Rental Property in Bankruptcy

If you are a rental property owner looking to escape financial ruin, contact a local bankruptcy attorney today. Our bankruptcy lawyers will help guide you in keeping your rental properties and lowering your debt through Chapter 13 bankruptcy.

How to live on a Chapter 13 Budget

A good attorney will present your case to the courts and get you a Chapter 13 budget that will be easy to follow and maintain.

The Pandemic Is Pushing Renters & Homeowners To The Brink

Filing for bankruptcy makes it possible for tenants to postpone any eviction proceedings through something called an “automatic stay”. Our Philadelphia bankruptcy attorneys can help you file for Chapter 7 or Chapter 13 bankruptcy.

4 changes to bankruptcies since the CARES Act you need to know

Filling for bankruptcy can seem scary, but our bankruptcy lawyers can help you navigate the 4 changes to bankruptcies since the CARES Act.

Philadelphia County is at risk for Foreclosures

There is now a large percentage of Americans at risk of financial instability.

Can bankruptcy save the American economy?

While bankruptcy tends to be a consumer’s last thought as an answer to their debt problems, some studies are now showing that debt relief programs may actually be the saving grace of our nation’s economy.

Debt too much to handle? (Get help against creditors)

During the current pandemic, people across the United States are struggling daily to deal with their ever-mounting bills. There is help you can seek now.

Can Creditors Take Your Stimulus Check?

Many of the nation’s most in-need families are likely to be in for a sad surprise when they realize that their check is far less than they had expected.

(Video) Radio 1210: A Conversation about the Stimulus and Debt Relief with Brad Sadek

Have any questions about your stimulus, creditors, or your financial options in these uncertain times? Watch (or read) the following conversation with attorney Brad Sadek as he answers all of the above.

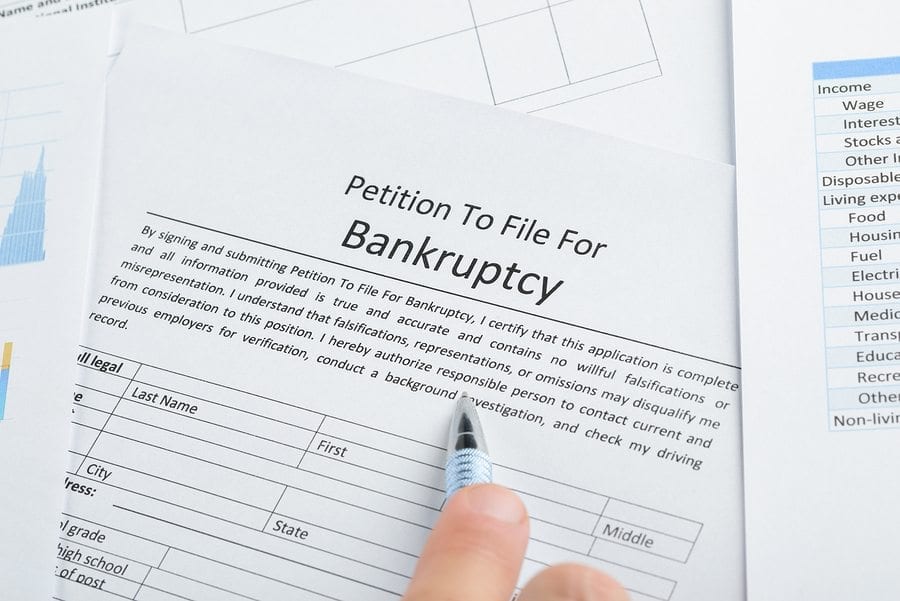

When Should You File for Bankruptcy

You may be thinking, is the middle of a pandemic really the best time to consider taking such a big step? Yes! If you are facing financial struggles the answer is most definitely sooner rather than later.

4 Advantages over Creditors in Bankruptcy

Like most areas of law, people do not want to file a bankruptcy proceeding, people file bankruptcy because they have to. There are several different types of Bankruptcy filings. The most common type of bankruptcy is consumer bankruptcy. Consumer Bankruptcies are filed on behalf of an individual or a married couple under Chapter 7 and […]

5 Post Bankruptcy Tips to Remain Debt Free

After filing bankruptcy, you can follow these 5 tips to remain debt free and continue enjoying your financial freedom.

Should I reaffirm my Mortgage Debt After Bankruptcy

The primary advantage of reaffirming a mortgage is accelerating an increase in credit score(s) after a bankruptcy discharge.