What Is a Personal Guarantee?

Navigating the complex terrain of financial obligations can often lead to moments of uncertainty, especially when personal guarantees are involved. At Sadek Bankruptcy Law Offices,

Navigating the complex terrain of financial obligations can often lead to moments of uncertainty, especially when personal guarantees are involved. At Sadek Bankruptcy Law Offices,

Understandably, many bankruptcy filers want to know what their potential tax consequences will be after they file. Bankruptcy can be the fresh start that people

Why Should You Never Pay a Debt Collection Agency? Navigating the murky waters of debt can be daunting, especially when collection agencies knock on your

Navigating the world of credit card debt can be daunting, especially when faced with the question: how much credit card debt is too much? At

Bankruptcy and FHA Loans: What You Need to Know An FHA loan is a mortgage loan that is insured by the Federal Housing Administration. It

How Long Does a Repo Stay on Your Credit? Navigating the aftermath of a repossession can be a daunting experience, fraught with uncertainties about its

A Court Ordered Judgment is actually towards the end of a legal cycle. Before a judgment is entered against a business entity or a person(s)

Can I file bankruptcy from home? Yes. Even before the COVID-19 pandemic, most of the Bankruptcy process could be completed without a visit to one of our

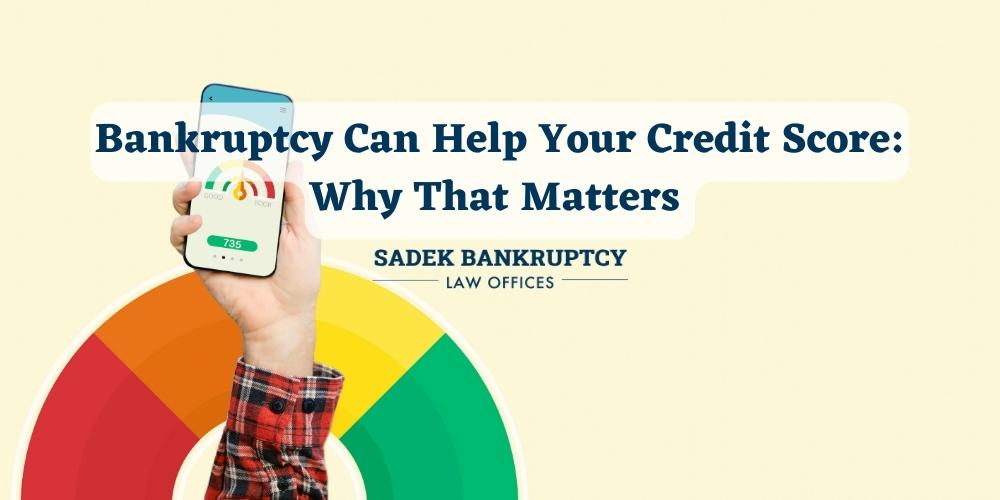

Bankruptcy Can Help Your Credit Score: Why That Matters One concern most people have when considering a bankruptcy is regarding the impact to their credit

It is extremely common to receive an inquiry from a bankruptcy filer that needs additional explanation or possibly a thorough review of their ongoing case

In today’s challenging economic landscape, the threat of losing one’s home due to foreclosure is a distressing reality for many homeowners. If you’re facing the

Steps to Rebuilding Your Credit Following a Bankruptcy in Philadelphia Filing for bankruptcy in Philadelphia provides you with a fresh start, but if not used

Filing bankruptcy in Philadelphia has many benefits and can help people in debt get back on track financially. There are numerous benefits of filing a

Bankruptcy is a legal process that helps people get rid of their debts and start over. It is designed to give consumers who are overwhelmed

Are you struggling to make mortgage payments and facing the possibility of losing your home in Philadelphia? You’re not alone. Many homeowners in Philadelphia face